Key Takeaways

- A serious synergy presentation is not a list of possible savings. It is a decision document that shows which synergies are real, what assumptions they depend on, how quickly they can be captured, and what price or integration choices they support.

- Cost, revenue, and capital synergies should not be collapsed into one number. Each has different evidence quality, timing, ownership, and credibility under diligence.

- The best synergy decks make the tradeoff visible between upside and execution risk. Executives should be able to see what is hard evidence, what is conditional, and what remains management ambition.

- AI should accelerate the first structured draft, scenario tables, and slide logic, but deal leaders still need to validate assumptions, challenge overlap estimates, and decide what belongs in the main story versus appendix.

Direct Answer: What An M&A Synergy Presentation Must Prove

An M&A synergy presentation must do three things at once. First, it has to show that the transaction creates real value beyond the standalone case. Second, it has to show that the value can actually be captured inside a realistic timeline. Third, it has to show that management understands the integration friction, one-time cost, and dependencies that sit between the model and the outcome. If any of those three layers are missing, the deck usually sounds optimistic rather than decision-ready.

That is why a synergy presentation is different from a generic acquisition deck. The audience is not only asking whether the target looks attractive. It is asking whether the combination economics justify the bid, whether the synergy pool is already embedded in the price, which levers can be realized with confidence, and where downside risk starts to erode the investment case. The page therefore needs tighter financial and operational discipline than a broad strategy narrative.

For corp dev teams, PE investors, bankers, CFOs, and operating partners, the useful standard is simple: can the audience understand the synergy logic by reading the slide titles, reviewing one bridge, checking one timing view, and seeing one explicit list of assumptions and risks? If not, the deck is still hiding too much reasoning in the spreadsheet.

Synergy Value-Capture Charter Reference

M&A Synergy Presentation Vs. Due Diligence Deck Vs. PMI Deck Vs. IC Memo

Synergy work often gets buried inside other deal materials. Use this comparison to decide what belongs in the dedicated synergy story.

| Artifact | Primary Question | What It Should Emphasize | Common Failure Mode |

|---|---|---|---|

| Synergy presentation | How much value is realistically available and what assumptions drive it? | Value bridge, timing, owners, dependency logic, supportable premium, and risk bounds | Headline number with no capture path |

| Due diligence deck | What did the team learn about the target and the deal risks? | Findings, red flags, workstreams, market context, and decision implications | Synergy upside buried after generic diligence commentary |

| PMI deck | How will the combined company execute after signing or close? | Workstreams, Day 1 continuity, milestones, integration governance, and business continuity | Planning detail with no tie back to value creation |

| Investment committee memo | Should the fund or company approve the deal and on what conditions? | Recommendation, valuation, risk, financing, thesis, and approval asks | Synergy case treated as a footnote to valuation |

Inputs To Gather Before Modeling Synergies

Why Most Synergy Slides Fail Before The Deal Closes

Most synergy slides fail because they confuse possibility with value that can actually be underwritten. Teams accumulate every overlap idea they can find, total the savings, and present a large number that looks impressive in a headline. That is usually the moment a serious audience becomes skeptical. Senior readers know that overlap is not the same as capture, and that theoretical overlap can disappear quickly once customer contracts, systems limits, regulatory constraints, or service-risk concerns become visible.

Another failure mode is mixing evidence quality. Some synergies are supported by identified headcount, site, or supplier data. Others depend on customer behavior, seller cooperation, or future product work that has not been validated yet. If the deck presents both categories as equally reliable, the model looks more precise than it really is. A better presentation explicitly separates hard cost actions, conditional execution levers, and strategic upside that is still narrative rather than committed.

The final failure is disconnecting synergy logic from deal price. Committees rarely care about synergy in the abstract. They care because synergy affects bid discipline, the supportable premium, the downside case, and the required pace of post-close execution. If the deck never makes that connection, it becomes a strategy appendix rather than a real decision tool.

Synergy Opportunity Segmentation Reference

Recommended 10-Slide M&A Synergy Presentation Sequence

This sequence works when the audience needs the synergy case itself, not a broad deal recap.

| Slide | Purpose | Executive Question Answered |

|---|---|---|

| Opening synergy thesis | State the total value range, confidence level, and key gating assumptions | Is there enough value here to matter? |

| Why the synergy case is credible | Explain the sources of overlap and where the case is strongest | Why should we believe the estimate? |

| Cost synergy bridge | Show the main buckets and what each one depends on | Where does the value come from? |

| Revenue synergy logic | Separate cross-sell, pricing, and retention levers from baseline growth | Which upside is operationally real versus story-level? |

| One-time cost and dis-synergy offsets | Bound the spend and disruption required to capture the value | What does it cost to get the savings? |

| Capture timing by year | Translate run-rate value into a realistic realization curve | When does the value arrive? |

| Supportable premium or underwriting impact | Link synergy NPV back to valuation discipline | How does this affect the price we can justify? |

| Top execution risks | Show what could delay or destroy the case | What breaks first if the plan slips? |

| Governance and owners | Name accountable leaders and escalation points | Who is actually responsible? |

| Decision asks and next steps | Specify what the audience must approve or challenge now | What action is required today? |

Prompt Recipe For An M&A Synergy Presentation

Create a 10-slide M&A synergy presentation for a corporate development, private equity, and CFO audience. Include an answer-first synergy thesis, cost and revenue synergy buckets, integration cost offsets, capture timing, supportable premium logic, top execution risks, named owners, and explicit decision asks. Separate hard synergies from conditional synergies, use consultant-style action titles, and keep the output editable in PowerPoint-style structure rather than decorative design.

Separate Hard Synergies, Conditional Synergies, And Story-Level Upside

A useful synergy presentation explicitly grades the evidence behind each value claim. Hard synergies are the ones where the overlap is identified, the mechanism is understood, and the organization can actually name the action required. Typical examples include procurement scale, duplicated corporate overhead, facility consolidation, or systems rationalization with a defined migration path. These should anchor the main valuation discussion because they are the most defendable.

Conditional synergies are different. They may still be very real, but they depend on choices, capacity, or timing that have not yet been fully proven. Cross-sell opportunities, pricing uplift, distribution leverage, or working-capital improvement often fall into this bucket. The deck should still show them, but it should label the dependency clearly: additional product work, customer-retention risk, sales coverage changes, integration sequencing, or regulatory approval. That makes the story credible without suppressing upside.

Story-level upside belongs in a separate lane. These are the strategic possibilities that may become true over a longer horizon but should not quietly justify today’s purchase price. Examples include accelerated platform expansion, new-market entry, or major product adjacency. A strong committee deck shows that management sees the upside, but it does not ask the underwriting case to depend on it.

Five-Phase Synergy Capture Timeline Reference

Action-Title Rewrite Matrix For Synergy Slides

The title should carry the judgment, not merely label the workstream.

| Weak Topic Title | Stronger Synergy Action Title | Why The Rewrite Works |

|---|---|---|

| Synergy overview | Most underwriteable value comes from procurement and overhead consolidation, not revenue upside | It tells the audience where the case is really coming from |

| Revenue synergies | Cross-sell upside is meaningful, but only after account coverage and packaging are redesigned | It separates value from the dependency that makes it real |

| Integration costs | One-time systems and people costs absorb the first-year savings, but not the full five-year value case | It frames the cost in the context that matters |

| Timeline | Only one-third of run-rate value should be treated as year-one capture under the current sequencing plan | It converts a schedule into a real underwriting implication |

| Risks | Customer and systems dependencies could delay revenue synergies even if cost actions remain on plan | It shows what risk affects, not just that risk exists |

| Next steps | Committee approval should be conditional on validating two overlap assumptions and one TSA cost item | It makes the decision ask precise and bounded |

Three-Phase Synergy Realization Plan Reference

Final Diligence Questions Before A Synergy Case Goes To Committee

Cost, Revenue, And Capital Synergies Need Different Evidence Standards

Use different proof standards for each category so the deck stays credible under scrutiny.

| Synergy Type | What The Slide Should Show | Minimum Evidence Standard |

|---|---|---|

| Cost synergy | Identified overlap, owner, timing, and expected run-rate savings | Bottom-up overlap logic, implementation requirement, and offsetting one-time cost |

| Revenue synergy | Named commercial lever, customer mechanism, and timing ramp | Evidence of attach rate, cross-sell path, pricing logic, or channel expansion feasibility |

| Capital synergy | Working-capital release, capex efficiency, or balance-sheet benefit path | Clear baseline and explanation of what operating change unlocks the capital benefit |

| Tax or financing benefit | Any transaction-structure or financing implication that affects realized value | Treasury, tax, or adviser-reviewed assumptions rather than generic deal folklore |

| Dis-synergy or offset | Temporary revenue drag, stranded cost, customer disruption, or TSA burden | Visible treatment in the main story, not hidden only in model notes |

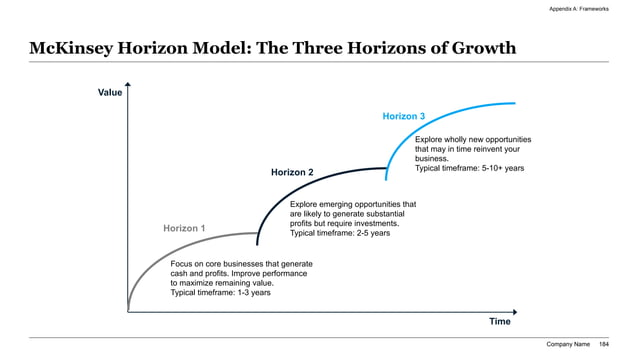

Three-Horizon Synergy Timing Reference

What AI Should Automate In The Synergy Workflow And What Deal Leaders Must Still Own

AI is valuable when it speeds up the repetitive parts of the synergy workflow. It can cluster diligence notes into synergy buckets, turn raw model outputs into a cleaner bridge, draft action-title options, summarize management interviews, structure risk tables, and turn a messy spreadsheet into the first coherent committee story. Those are meaningful productivity gains because synergy work is often assembled under heavy time pressure across bankers, corp dev, finance, and operating teams.

What AI should not own is the underwriting judgment. A model cannot decide whether procurement overlap is truly addressable, whether commercial teams can cross-sell without hurting retention, or whether a systems consolidation plan is realistic under customer and regulatory constraints. It also should not decide how much of the synergy value deserves to be paid away in price. Those are management and investor judgments, not formatting tasks.

For XLSlides, the right product promise is speed with structure. The platform should help the user move from memo, diligence tracker, and model notes to an editable first draft with action titles, bridge logic, and value-capture sections already organized. The final deck still needs an experienced human to validate every major assumption before it goes to an IC, board, or financing audience.

XLSlides Resources For Synergy, Deal, And Approval Work

Short Answers To Common Synergy Presentation Questions

How is an M&A synergy presentation different from a PMI deck?

A synergy presentation proves the value available in the combination and the assumptions required to capture it. A PMI deck is the broader execution plan after signing or close. The PMI deck includes workstreams, Day 1 continuity, and integration governance; the synergy deck is narrower and more directly tied to price, underwriting, and value creation.

What belongs in the main synergy deck instead of appendix?

The main story should carry the headline value range, cost and revenue synergy logic, offsets, timing, supportable premium impact, major risks, and accountable owners. Appendix should hold detailed overlap schedules, customer lists, benchmark support, and lower-priority sensitivity cases.

Should revenue synergies be shown alongside cost synergies?

Yes, but not as if they have the same certainty. Revenue synergies often depend on commercial execution and customer behavior, so the slide should separate them from harder cost actions and label the assumptions more explicitly.

Can AI create a credible synergy presentation?

Yes, as a drafting layer. AI is useful for structuring the first story, drafting tables, rewriting headlines, and converting model outputs into a cleaner deck. The final version still needs deal-team judgment on overlap, capture feasibility, pricing discipline, and disclosure sensitivity.

Build The First Synergy Case In XLSlides

Use XLSlides to turn diligence notes, overlap assumptions, integration costs, and synergy model outputs into an editable M&A synergy presentation with action titles, value bridges, timing logic, and a clearer decision path for committees and boards.

Generate Synergy Deck