Valuation Deck Takeaways

- A valuation presentation is a decision document about range, assumptions, and confidence, not just a spreadsheet summary.

- The first slides should show what the business may be worth, why that range is credible, and which assumptions would move it materially.

- Strong decks separate method choice, peer evidence, scenario sensitivity, and the enterprise-to-equity bridge instead of hiding them in appendix math.

- Executives will challenge the peer set, normalization adjustments, discount rate, downside case, and the exact implication for price or action.

- AI is useful when it turns comps, models, notes, and diligence findings into a structured first draft that still remains editable for finance review.

Direct Answer: What A Valuation Presentation Must Do

A valuation presentation should help a senior reader answer three questions quickly: what is the asset or business worth, why is that range credible, and what should we do with that conclusion? That last question matters more than many teams admit. A board finance committee may need to decide whether a proposed acquisition price is still defensible. A private equity deal team may need to confirm whether the return case survives diligence. A CFO may need to explain why the company's internal value view differs from the public market narrative. If the deck cannot connect the math to the decision, it will feel incomplete no matter how polished the charts look.

The best valuation decks therefore treat the model as supporting evidence, not as the whole story. They show the logic behind the range, the peer set, the key revenue and margin drivers, the bridge from enterprise value to equity value, and the scenario changes that matter most. They also make clear where judgment enters the process. A single point estimate is rarely the real answer. The real answer is usually a range conditioned by assumptions, comparables, capital structure, timing, and risk.

For XLSlides, the product fit is straightforward. Finance teams already have messy raw material: DCF tabs, EBITDA bridges, precedent transaction notes, board comments, and diligence findings. The time sink is turning that material into a coherent slide draft with action titles, clean valuation exhibits, and PowerPoint-style editability. The tool should accelerate the mechanics while leaving the final assumptions, range selection, and disclosure judgment with the human owner.

When Teams Actually Need A Valuation Deck

Different valuation situations require different decision framing. The deck should match the audience and the exact valuation question, not just restate the model output.

| Situation | Decision Needed | What The Deck Must Prove | What Reviewers Challenge First |

|---|---|---|---|

| Board valuation review | Is management's range still supportable for planning, financing, or strategic decisions? | Why the current value view fits operating performance, market conditions, and capital structure | Whether the range is stale, optimistic, or disconnected from current performance |

| Buy-side investment committee | Should we approve the bid or revise price expectations? | Why the business quality, downside protection, and return bridge justify the entry valuation | Whether the upside depends on fragile assumptions or generous exit multiples |

| Sell-side management preparation | How should we frame the value story for buyers or advisers? | What supports the high case and what risks need controlled disclosure | Whether normalization and growth claims can survive buyer diligence |

| Corporate development screening | Is the target worth deeper work or should it be deprioritized? | Whether the business clears strategic and financial thresholds before full diligence | Whether the initial range ignores integration cost or risk concentration |

| Capital allocation review | Should we deploy capital here instead of to the alternatives? | How the return case compares with internal hurdle rates and other uses of capital | Whether WACC, cost of equity, or downside assumptions are being treated too lightly |

| Fundraising or investor narrative | How do we explain the value logic without turning the deck into spreadsheet theater? | Why the market opportunity, unit economics, and scenario path support the stated valuation narrative | Whether the story overreaches relative to traction, margin profile, or cash needs |

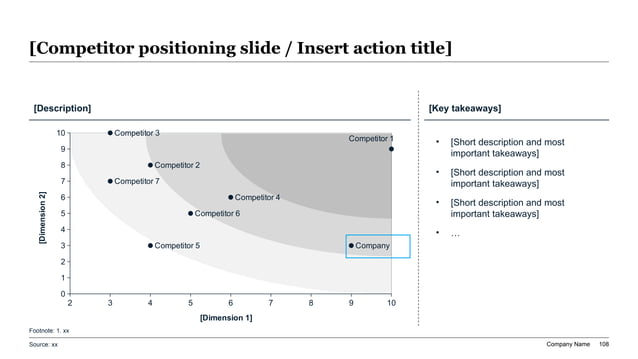

Peer Positioning Landscape Reference

Which Valuation Method Belongs In The Main Story

Not every method deserves equal airtime in the core deck. Lead with the method that best matches the decision and keep secondary support visible but subordinate.

| Method | Best Use In A Presentation | What The Slide Must Show | Common Failure Mode |

|---|---|---|---|

| Trading comps | Board reviews, quick screening, public-market triangulation | Peer set logic, metric definitions, multiple range, and why the business should sit where it does | Using a weak peer set and then treating the median multiple as objective truth |

| Precedent transactions | M&A context, sponsor or adviser discussions, market-clearing references | Why the chosen deals are truly comparable on timing, sector, scale, and control premium | Mixing old cycle transactions with current trading conditions without explanation |

| DCF | Capital allocation, strategic reviews, downside cases, long-duration assets | Revenue and margin logic, cash conversion, WACC or cost of equity assumptions, and sensitivity bands | Presenting a precise point estimate while burying the assumptions that create it |

| Sum-of-the-parts | Conglomerates, carve-outs, or businesses with clearly distinct economics | How each segment is valued and what the corporate costs or dis-synergies do to equity value | Adding segment values cleanly while ignoring holdco drag or stranded cost |

| Scenario range | Uncertain outlooks, turnaround cases, cyclical names, approval debates | What changes between base, upside, and downside and how that affects the range | Renaming slight assumption tweaks as separate scenarios |

| LBO or sponsor return framing | PE committee debates, bid discipline, leverage-sensitive cases | Entry price, debt capacity, value-creation path, exit assumptions, and return threshold | Relying on financial engineering when the operating case is still weak |

Start With The Valuation Question Before You Open Excel

Teams often begin valuation work inside the model and only later ask what the presentation needs to achieve. That order is backwards for executive communication. Before opening the workbook, define the decision. Are you defending an internal fair-value range, approving an acquisition price, screening a target, or explaining why management believes the public market is missing something? Each question changes the slide sequence, the choice of exhibits, and the standard of proof.

A buy-side committee deck, for example, should not spend most of its energy on generic market background if the real challenge is underwriting the downside and the exit assumptions. A board valuation review should not look like an adviser pitch. It should focus on how operating performance, peer positioning, capital structure, and sensitivity ranges affect the board's judgment. A founder or CFO investor deck may need a more selective value narrative, but it still has to make the logic behind the range understandable. The audience decides what belongs in the main flow versus the appendix.

This framing also makes AI outputs materially better. When the prompt specifies audience, valuation methods in scope, the exact decision, the acceptable range, the main value drivers, and which assumptions the audience is likely to challenge, the first draft becomes useful. Without that framing, AI tends to produce generic finance slides that sound intelligent but do not answer the actual valuation question.

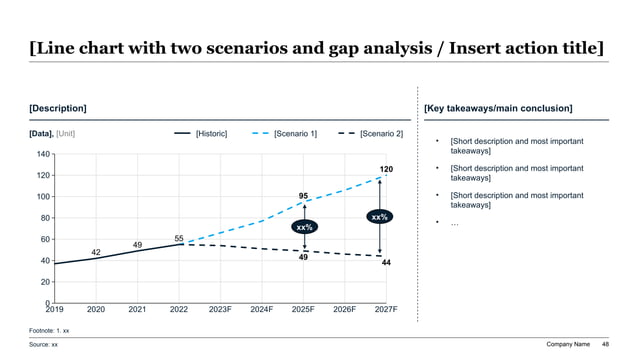

Scenario Gap Analysis Reference

Recommended 12-Slide Valuation Deck Sequence

| Slide | Purpose | Skeptical Question It Answers |

|---|---|---|

| Executive valuation summary | State the range, recommendation, and what drives it | What is the answer before I read the details? |

| Decision frame | Explain why the valuation matters now | Why is this being discussed now and what action follows? |

| Business quality snapshot | Summarize the operating profile that supports value | What kind of business are we valuing? |

| Peer set and market positioning | Show which comparables matter and why | Why should I trust these peers? |

| Trading comps output | Translate peers into a defensible multiple range | Where should this asset trade relative to the set? |

| DCF or intrinsic value view | Show cash flow logic and discount-rate assumptions | What is the value if market multiples mislead us? |

| Enterprise-to-equity bridge | Convert headline value into what equity holders actually get | How do debt, cash, and adjustments change the answer? |

| Scenario and sensitivity range | Pressure-test the valuation under key assumptions | What happens if growth, margin, or WACC moves? |

| Normalization and adjustments | Explain EBITDA or cash-flow cleanups | Are we valuing real earnings or adjusted fiction? |

| Risks and value detractors | Surface what could compress the range | What are we underestimating? |

| Implication and negotiation stance | Turn the valuation into a price, reserve, or decision boundary | So what should we do with this range? |

| Appendix and source notes | Preserve model detail, peer tables, and formulas | Where can the finance team verify the support? |

Action Title Rewrite Matrix For Valuation Slides

A useful valuation deck tells the reader what to conclude from the number, not just what calculation sits on the page.

| Weak Topic Title | Stronger Valuation Title | Why The Rewrite Works |

|---|---|---|

| Trading comps | Peer multiples imply a 9.5x to 11.0x EBITDA range, with the business likely sitting at the upper half because retention and margin profile exceed the peer median | It turns raw market data into a reasoned placement inside the range |

| DCF analysis | Intrinsic value remains above the current bid unless margin expansion slips by more than two years | It states the implication and the assumption that matters most |

| Sensitivity | WACC and terminal growth explain most of the downside, while minor working-capital changes do not move the decision | It separates material sensitivity from spreadsheet noise |

| Adjustments | One-time restructuring costs should be normalized, but recurring customer-support spend should remain in run-rate EBITDA | It signals judgment instead of hiding behind a generic adjustment label |

| Scenario analysis | The downside case still supports price discipline, but not the original stretch multiple | It converts scenario math into decision language |

| Recommendation | Management should defend value within the stated range and avoid paying for the upside case upfront | It gives the audience an explicit negotiating or approval stance |

Prompt Recipe For A Valuation Presentation

Create a 12-slide valuation presentation for a CFO, corporate development lead, and investment committee evaluating a potential acquisition of a mid-market B2B software company. Include an answer-first valuation summary, decision frame, business quality snapshot, peer set logic, EV/EBITDA comps, DCF support with WACC assumptions, enterprise-to-equity bridge, scenario and sensitivity range, EBITDA normalization notes, key risks, recommended price posture, and appendix placeholders for source notes. Use consultant-style action titles, make every chart explain what changes the range, and keep the output editable in PowerPoint style rather than decorative.

Build The Equity Story, Not Just The Math

Many valuation decks stop at enterprise value and assume the audience will mentally translate that into a real equity conclusion. Serious readers do not want that burden. They want to see how the headline value becomes an equity range after debt, cash, working-capital adjustments, minority interests, one-time costs, or other claims are applied. This is where otherwise strong models often lose credibility in presentation form. If the deck makes a company look attractive only before the bridge to equity reality, the audience will notice quickly.

A useful valuation presentation also distinguishes between business quality and valuation mechanics. A higher multiple or stronger DCF result should flow from something visible in the story: more resilient margins, cleaner retention, better cash conversion, stronger market structure, or more credible execution. If the range is simply asserted because the company feels premium, the audience will treat the conclusion as advocacy. Peer positioning, operating evidence, and scenario discipline are what convert the model into a defendable narrative.

The practical standard is simple. A reader should be able to scan the slide titles, inspect the bridge, and understand why the recommended price range is what it is and what could move it up or down. That is what turns valuation from an analyst output into an executive document.

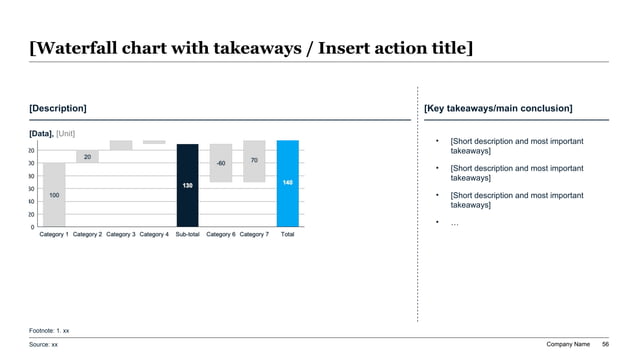

Enterprise-To-Equity Bridge Reference

Questions Sophisticated Reviewers Will Ask

Source Discipline By Valuation Slide Type

The strongest valuation decks make the evidence chain obvious. Every important number should be traceable without turning the main pages into raw spreadsheet dumps.

| Slide Type | Evidence Needed | Minimum Source Standard |

|---|---|---|

| Peer set and market positioning | Public filings, consensus data, defined metric windows, and selection rationale | Name the source system or filing basis and disclose why each peer belongs |

| Trading multiple table | Enterprise value date, EBITDA or revenue basis, and normalization notes | State the valuation date and metric definition so ratios are comparable |

| DCF summary | Revenue build, margin path, capex, working capital, and discount assumptions | Show the variables that move the range, not only the final output |

| Enterprise-to-equity bridge | Net debt, cash, minority interests, leases, and other adjustments | Tie back to the balance sheet date and note any management adjustments |

| Scenario sensitivity | Clear changes by case and the reason those changes are plausible | Show what changes and what remains fixed across scenarios |

| Normalization slide | One-time items, owner adjustments, and accounting or operational rationale | Make the judgment explicit instead of hiding it inside a model footnote |

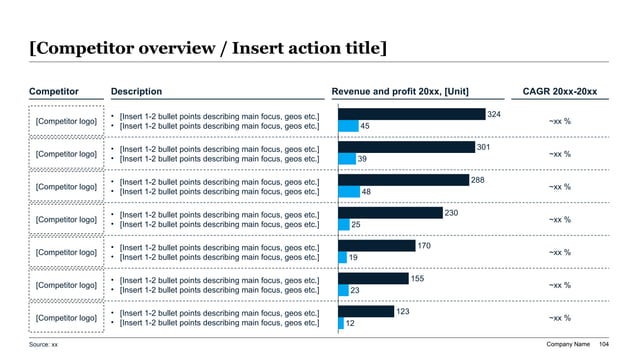

Peer Revenue And Profit Comparison Reference

What AI Should Automate In Valuation Workflows

AI can remove a surprising amount of mechanical work from valuation decks. It can organize comps notes, turn model outputs into a suggested storyline, draft action titles, propose where the bridge or sensitivity should appear, convert long diligence comments into shorter risk statements, and build the first version of a board-ready or IC-ready slide sequence. That matters because most finance teams do not struggle with the existence of data. They struggle with converting that data into a coherent presentation before the review deadline.

What AI should not own is the judgment layer. It should not decide the peer set, normalize EBITDA without owner review, select the final WACC range without context, or choose which scenario is the true base case. It also should not smooth over disagreements. In many live valuation workflows, the important work is precisely the disagreement: which assumptions are credible, which risks deserve valuation penalties, and which adjustments can be defended in front of a committee or adviser.

The right promise for XLSlides is therefore modest and strong at the same time. It can create the serious first draft that turns models, notes, and comments into an editable slide file. Finance leaders still own the economic truth. That division of labor is exactly what sophisticated users want.

Reviewer Lens By Audience

The same valuation output should not be presented the same way to every audience. Tailor the narrative to what each group actually needs to decide.

| Audience | What They Care About Most | What To Avoid |

|---|---|---|

| Board finance committee | Whether the range is prudent, current, and decision-useful for capital allocation or governance | A dense banker-style appendix masquerading as the main story |

| Private equity investment committee | Entry discipline, downside protection, leverage tolerance, and exit realism | An upside-heavy narrative that assumes multiple expansion without proof |

| Corporate development lead | Whether the target clears strategic fit and financial thresholds before deeper spend | Early precision that ignores integration cost or execution complexity |

| CFO and executive sponsor | What range is defendable internally and externally, and how assumptions tie to operations | Treating valuation as a standalone finance exercise with no operating narrative |

| Adviser or lender audience | Consistency, downside durability, and what evidence is truly supportable in diligence | Hand-waving through sources, normalization, or capital structure detail |

| Founder or investor-update audience | Whether the value story is credible relative to traction, cash needs, and market comparables | Pitch language that outruns the metrics and erodes trust |

Decision Tree And Range Framing Reference

Short Answers To Common Valuation Deck Questions

What should be on the first slide of a valuation presentation?

The first slide should state the valuation range, what decision the audience needs to make, the main methods supporting the range, and the two or three assumptions that matter most. A senior reader should not need to flip through ten pages before learning whether management believes the business is worth 8x EBITDA or 11x, or whether the recommended posture is to defend the current range, walk away, or negotiate down. If the opening summary hides the range, the deck usually feels less confident than the underlying analysis.

How do you choose between DCF and comps in an executive deck?

Use the method that best answers the decision and then keep the other method visible as a cross-check. Trading comps are often the fastest way to anchor a current market conversation. DCF is useful when the operating path, capital allocation logic, or long-duration cash flow matters enough that current multiples alone are too shallow. In most serious decks, the argument is not DCF versus comps. It is which method leads and which method validates the range.

How much model detail belongs in the main presentation?

Enough to make the logic auditable, but not so much that the deck becomes a workbook export. The main flow should show the value drivers, peer set, assumptions that move the range, and the enterprise-to-equity bridge. Detailed formulas, long peer tables, and supporting sensitivity tabs belong in the appendix. The test is simple: can the audience understand why the range is what it is without reading hidden spreadsheet logic, and can the finance team still defend every material number when challenged?

Can AI build the first draft of a valuation deck?

Yes, if the inputs are structured and the team treats AI as a drafting system rather than a valuation authority. XLSlides can turn model outputs, peer notes, diligence comments, and decision context into an initial slide sequence with action titles, summary language, bridge logic, and chart placeholders. The final range, adjustments, scenario selection, and disclosure choices still need human review. Sophisticated users do not want AI to replace judgment. They want it to compress the time between analysis and a presentable first draft.

Turn The Valuation Logic Into An Editable Deck

Use XLSlides to turn model outputs, peer tables, diligence notes, WACC assumptions, and price discussions into an editable valuation presentation with action titles, scenario views, bridge exhibits, and PowerPoint-ready structure.

Generate Valuation Deck