Key Takeaways

- A zero-based budgeting presentation is a decision document about resource allocation, not a generic annual budget readout.

- The opening slide should show where spend can move, what must be protected, and what leadership needs to approve now.

- Strong ZBB decks tie every cost challenge to business logic, owner accountability, and an explicit reinvestment or margin implication.

- AI is useful when it turns raw budget notes, category analysis, and workshop outputs into an editable first draft without pretending to replace finance judgment.

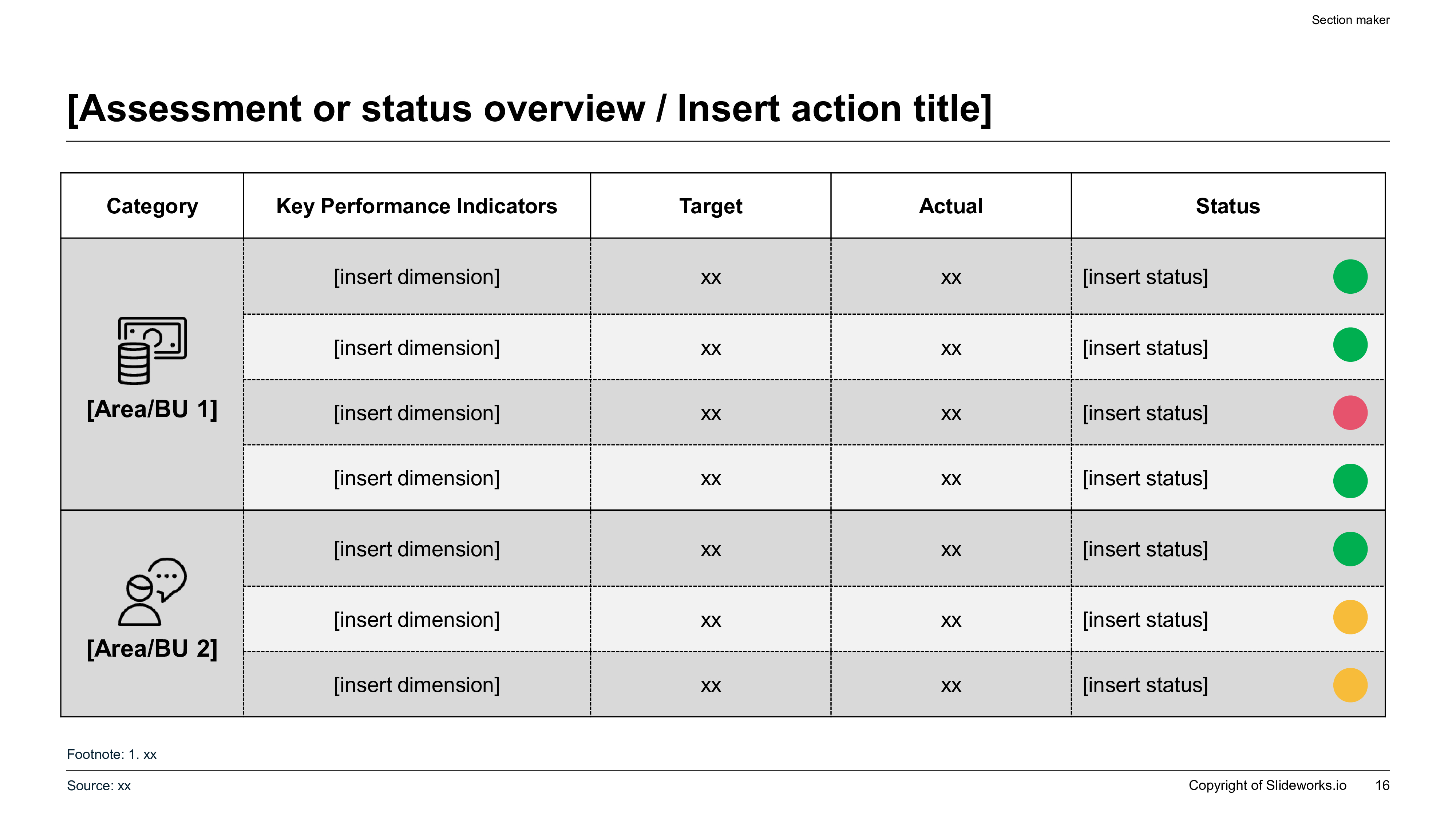

Category Review Scorecard Reference

What A Zero-Based Budgeting Presentation Needs To Do

A zero-based budgeting presentation has a narrower and more demanding job than a standard annual planning deck. It must show that leadership has challenged spend from the ground up, separated necessary investment from historical carry-forward, and made deliberate tradeoffs about what the business should fund, redesign, reduce, or stop. If the deck simply repeats the old budget in new colors, it has missed the point.

Senior audiences also expect the deck to answer two questions quickly. First, where is the money today and why is it there? Second, what changes if the company truly budgets from zero rather than defending last year's baseline? The useful output is not a larger spreadsheet appendix. It is a boardroom-ready narrative that connects category decisions to growth, margin, service levels, capability building, and execution risk.

That is why this topic fits XLSlides well. Finance teams often have the analysis but not the presentation workflow. They have cost-center exports, workshop notes, benchmark findings, ownership gaps, and scenario models scattered across spreadsheets and documents. What they need next is a clear storyline with action titles, evidence modules, source-note discipline, and editable PowerPoint-style output.

When To Use A Zero-Based Budgeting Deck

The same presentation structure should not be used for every finance review. ZBB matters most when leadership is making explicit funding tradeoffs rather than just reporting budget status.

| Situation | Decision Leadership Needs | What The Deck Should Emphasize |

|---|---|---|

| Cost reset after slower growth | Which costs should be removed, redesigned, or protected? | Baseline challenge, savings potential, business impact, and speed to capture |

| Margin improvement program | Where can the company free up dollars without breaking execution? | Category logic, owner accountability, and reinvestment versus flow-through choices |

| Private equity value-creation plan | Which SG&A and operating costs need immediate action? | Rapid diagnostic, benchmark gaps, initiative prioritization, and governance cadence |

| Planning cycle redesign | Should the company adopt ZBB principles in the next budget year? | Operating model, workload tradeoffs, tools, and where full ZBB is worth the effort |

| Board or sponsor review | What actions require approval and what risks must be accepted? | Decision asks, savings bridge, protected investments, and execution guardrails |

What Executives Want Answered In The First Five Minutes

How A Serious ZBB Storyline Differs From A Normal Budget Update

A standard budget presentation often starts with historical actuals, then moves into next-year assumptions, then ends with a variance bridge. A zero-based budgeting deck should reverse that logic. Start with the conclusion: which spending pools were challenged, what the analysis found, and what leadership should do because of those findings. The audience is not waiting to be educated on the existence of overhead costs. It wants a recommendation.

That recommendation should usually separate three buckets. First, spend that must be protected because it underpins compliance, revenue generation, safety, or strategic capability. Second, spend that can be redesigned through policy, process, sourcing, automation, or demand management. Third, spend that should be reduced or stopped because it no longer clears the value threshold. This three-bucket logic keeps the discussion from collapsing into generic cost cutting.

The deck should also show that ZBB is not just a finance exercise. Good zero-based budgeting work changes behavior. It clarifies who owns indirect spend, which service levels are actually required, where demand for internal work should be governed more tightly, and where historic budget entitlements have survived without challenge. That broader operating implication is what makes the deck useful to senior management.

Scenario-Based Budget Choice Visual

Recommended 12-Slide Zero-Based Budgeting Deck

| Slide | Purpose | Executive Question Answered |

|---|---|---|

| Executive summary | State the funding recommendation and decision asks | What should we approve? |

| Why now | Show the business context for challenging spend | Why is a baseline reset required? |

| Scope and baseline | Define spend in scope by category and owner | What dollars are we actually reviewing? |

| Method and design principles | Explain how categories were challenged from zero | How rigorous was the review? |

| Category findings | Summarize where the biggest opportunity sits | Where are the largest gaps? |

| Protected spend | Show what cannot be cut without harm | What must stay funded? |

| Savings bridge | Convert category actions into dollars and timing | How much is credible and when? |

| Reinvestment choices | Show where savings should be redeployed | What should we fund instead? |

| Risks and service-level implications | Surface downside and mitigation | What could break if we move too fast? |

| Operating model and governance | Assign decision rights and control points | Who owns enforcement? |

| 90- to 180-day roadmap | Sequence actions and milestones | How do we implement this? |

| Appendix and source notes | Preserve assumptions and category detail | Where is the proof? |

Direct Answer: What Should Be On A Zero-Based Budgeting Presentation First Slide

The first slide should state the answer, not the process. A strong opening summary says how much spend was reviewed, what level of savings or reallocation is credible, which investments should remain protected, and which approvals leadership needs to make now. If a reader can only scan one page, that page should still explain the recommendation, the reason it is credible, and the consequence of delay.

In practice, that means the first slide usually combines four elements: a one-sentence recommendation, a small savings or reallocation bridge, two to four supporting proof points, and a short list of decisions or guardrails. That structure is more useful than a generic headline such as Budget Review or Cost Program Update because it tells the audience what to conclude before they enter the detail.

Prompt Recipe For A Zero-Based Budgeting Deck

Create a zero-based budgeting presentation for the CFO, CEO, business unit leaders, and board finance committee. Company context: a mid-market B2B services business with slowing revenue growth and margin pressure. Objective: challenge SG&A and selected operating costs from zero, protect customer-critical and compliance-critical spend, identify credible savings and reinvestment opportunities, and define the governance model. Include an answer-first executive summary, why-now framing, spend-in-scope baseline, category findings by owner, protected spend logic, savings bridge, scenario comparison, reinvestment choices, service-level and execution risks, governance design, 180-day roadmap, and explicit approval asks. Use consulting-style action titles, show where assumptions are directional, and keep the output editable in PowerPoint style.

Savings Bridge Reference

Action Title Rewrite Matrix For ZBB Slides

Zero-based budgeting decks lose force when slide titles are only labels. The title should state the implication of the category review.

| Weak Topic Title | Executive Action Title | Why The Rewrite Works |

|---|---|---|

| Travel and events | Commercial travel can be reset without harming growth if approval thresholds and internal event design change together | It turns a cost bucket into an operating conclusion |

| Technology spend | Software savings are real, but most value depends on retiring redundant tools rather than negotiating licenses alone | It separates superficial savings from structural change |

| Org structure | Management layers can be simplified in support functions, but customer-facing coverage should stay protected | It makes the protection logic visible |

| Marketing | Low-yield brand and agency spend should be reallocated to proven demand programs instead of cut uniformly | It frames reallocation, not blind reduction |

| Procurement | Category ownership and intake discipline are now the gating factors for sustaining savings | It surfaces the execution bottleneck |

| Next steps | Leadership should approve category owners, service-level guardrails, and the first-wave savings plan this month | It tells the audience exactly what decision is required |

How To Build The Category Logic Without Creating A Spreadsheet Cemetery

One of the most common ZBB failure modes is showing every category with the same level of detail. That produces a dense appendix but a weak executive story. The better approach is to group categories by decision type. Some categories need redesign because demand is poorly governed. Some need sourcing or vendor consolidation. Some need service-level challenge. Some should be protected because they are already lean or strategically important. This classification produces a clearer main narrative than a flat list of cost centers.

The second discipline is to separate gross ideas from net actionable savings. If a category shows a large benchmark gap but closing that gap would force unacceptable service degradation, the deck should say so clearly. Senior readers trust transparent tradeoffs more than inflated savings numbers. The point of the presentation is not to make the biggest claim. It is to show which dollars can move with confidence.

Finally, every category should have a human owner. A deck without ownership drifts back into annual budgeting habits. Showing owner, decision needed, and evidence quality beside each category is often more valuable than showing another decimal place.

Category Review Questions Before A Slide Makes The Main Story

ZBB Workstreams And The Evidence Each One Needs

Credible zero-based budgeting work uses different proof types for different cost categories.

| Workstream | Typical Opportunity | Minimum Evidence Standard |

|---|---|---|

| Third-party spend | Vendor consolidation, rate reset, scope reduction | Contract inventory, spend cube, renewal timing, usage challenge |

| People and layers | Span simplification, role redesign, duplicate activity removal | Org maps, workload logic, service expectations, transition constraints |

| Internal demand management | Lower meeting, travel, reporting, or approval friction | Demand volumes, policy leakage, exception data, stakeholder interviews |

| Technology and tools | License rationalization, app retirement, workflow automation | Application inventory, license usage, business owner validation, migration risk |

| Marketing and discretionary programs | Reallocation from low-yield spend to proven initiatives | Channel performance, CAC or payback logic, strategy priorities |

| Facilities and operating overhead | Footprint reset, shared-service redesign, policy change | Occupancy data, utilization, contractual obligations, timing of exit |

Governance Ownership Tree

What To Automate In The ZBB Workflow And What To Keep Human

AI should automate the repetitive translation layer around zero-based budgeting: turning workshop notes into draft slide titles, mapping category findings into a consistent deck structure, rewriting rough comments into clearer executive language, and proposing first-pass visuals for scorecards, bridges, and roadmaps. Those tasks consume a lot of finance and consulting time but do not require final decision authority.

What AI should not own is the truth status of the savings case. It does not know whether a service-level assumption is politically acceptable, whether a benchmark is genuinely comparable, whether a vendor can be exited inside the time window, or whether a protected category is actually over-defended by management. Those are judgment calls that belong to the CFO, FP&A lead, operating partner, or workstream owner.

That line matters for product positioning. XLSlides should not promise instant cost-transformation truth from a vague prompt. The stronger promise is practical: faster deck assembly, clearer narrative structure, better action titles, and a cleaner editable first draft that serious finance teams can pressure-test before the meeting.

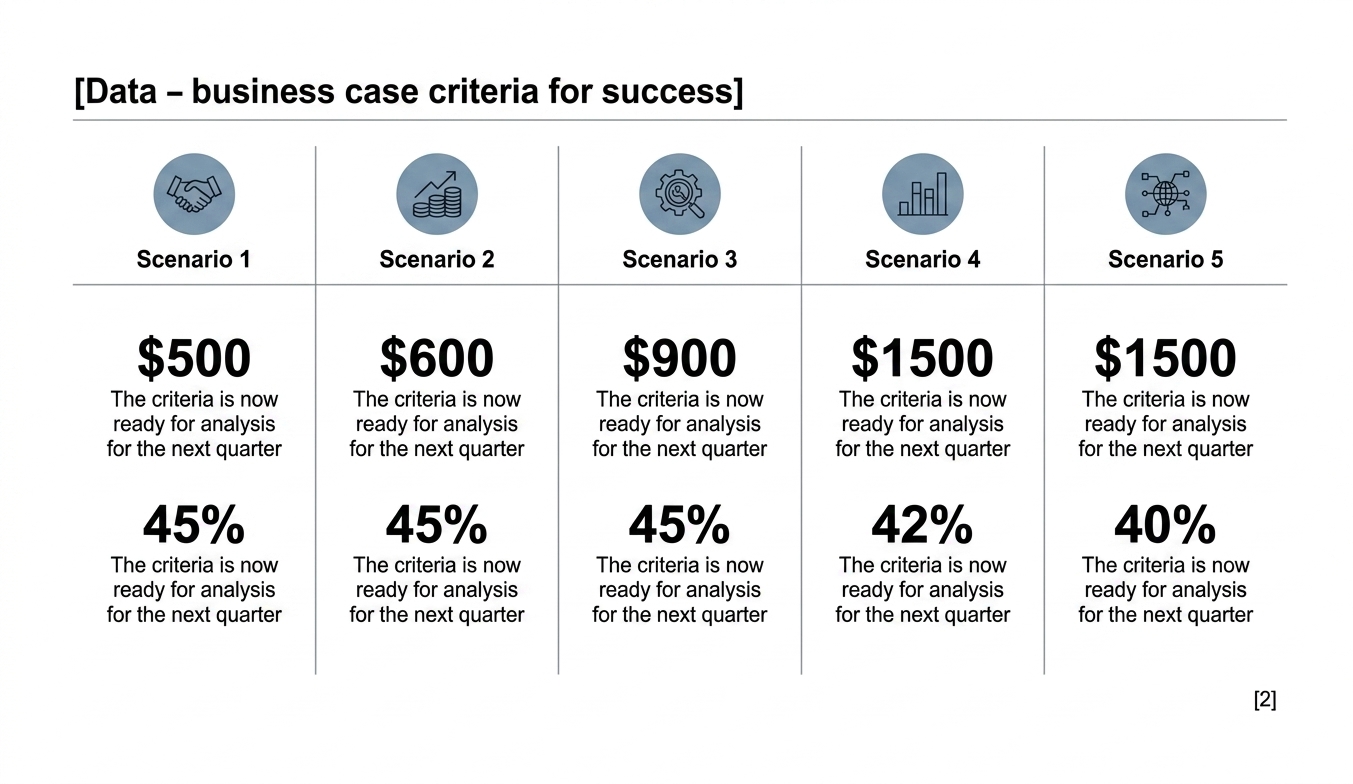

Scenario Comparison Framework For Finance Leadership

ZBB decisions are easier when the deck frames distinct options rather than one all-or-nothing answer.

| Scenario | What Changes | When It Makes Sense |

|---|---|---|

| Light-touch challenge | Focus on top spend categories, vendor resets, and policy tightening | Useful when leadership needs quick savings with limited organizational disruption |

| Targeted zero-base redesign | Rebuild selected functions or categories from zero with owner accountability | Best when margin pressure is real but a full enterprise reset is too heavy |

| Enterprise-wide ZBB program | Challenge broad SG&A and operating-support spend across the company | Appropriate when the company needs a durable cost reset and governance change |

| Reallocation-led ZBB | Use savings mostly to fund growth, systems, or capability priorities | Best when the business needs to protect strategy while raising resource quality |

| Sponsor-led rapid intervention | Run a shorter, high-accountability wave tied to value-creation milestones | Useful in PE-backed or turnaround contexts where timing matters more than elegance |

Mistakes That Make A ZBB Deck Unconvincing

Implementation Roadmap Reference

Short Answers To Common Zero-Based Budgeting Questions

What is the difference between a zero-based budgeting presentation and a normal budget presentation?

A normal budget presentation usually explains next-year assumptions against the prior baseline. A zero-based budgeting presentation challenges the baseline itself, shows which spend should be protected or reset, and turns that analysis into explicit funding decisions.

What should a CFO put on the first slide of a ZBB deck?

The first slide should show the recommendation, the dollars in scope, the credible savings or reallocation range, the protected investments, and the decisions leadership needs to approve now.

How many categories should appear in the main story of a zero-based budgeting deck?

Usually only the categories that drive most of the value or most of the risk. The main narrative should summarize the few areas that matter most, while detailed subcategories and calculations can move to the appendix.

Can AI create a credible zero-based budgeting presentation?

Yes, if AI is used to structure notes, draft action titles, and build the first-pass deck. Human reviewers still need to validate the evidence, challenge assumptions, and decide whether savings are truly achievable.

The Review Standard Before You Send The Deck

Before circulating the deck, read only the action titles. They should tell the story of the budget reset without needing the charts. If the headlines read like category names rather than conclusions, the deck is still too close to spreadsheet reporting.

Then test the evidence. Every major dollar claim should trace back to a contract fact, benchmark, usage pattern, service-level choice, or named management judgment. If the team cannot explain why a number is credible, that line should not sit in the executive summary.

Finally, test the operating realism. Good ZBB decks do not simply maximize savings on paper. They show which controls, owners, and sequencing choices will make the budget behave differently after the meeting. That is the threshold between a presentation and an actual management mechanism.

Draft The Zero-Based Budgeting Deck In XLSlides

Use XLSlides to turn category analyses, budget notes, benchmark findings, and CFO working papers into an editable zero-based budgeting presentation with action titles, savings bridges, governance logic, and PowerPoint-style output.

Generate ZBB Deck